Real Estate Blog

To Buy Now or Latter - Expert Analysis

I once met an experienced real estate investor who said to me the best time to buy is when you are ready, and I agreed with her assertion. ...

READ POSTI once met an experienced real estate investor who said to me the best time to buy is when you are ready, and I agreed with her assertion. ...

READ POSTYou may have been thinking of selling your house this spring, now is the perfect time to start getting it ready. With the market gearing ...

READ POSTAs the weather warms up and flowers begin to bloom, the real estate market traditionally sees an uptick in activity during the spring ...

READ POSTThe First-Time Home Buyer Incentive helps qualified first-time homebuyers reduce their monthly mortgage payments without adding to ...

READ POST

I once met an experienced real estate investor who said to me the best time to buy is when you are ready, and I agreed with her assertion. Everyone's opinion may differ on this matter and this is why I would like to consider a case study in this blog.

Report has shown that Many People are Waiting as at spring 2024 for the bank of Canada to reduce rates before hopping into the market

Consider a buyer looking at a $300,000 home with a 4% interest rate today. They decide to wait, expecting rates to drop to 3.5% next year. If the home appreciates by 7%, it would be worth $321,000. Here’s a comparison:

Current Scenario (4% rate):

Loan Amount: $240,000 (assuming 20% down payment)

Monthly Payment: $1,145

Future Scenario (3.5% rate, $321,000 home):

Loan Amount: $256,800 (assuming 20% down payment)

Monthly Payment: $1,154

Despite the lower rate, the higher home price results in a higher monthly payment, illustrating how waiting can lead to negligible or negative financial benefits.

I would advise buyers to conduct a thorough financial analysis. Tools like Mortgage Calculator can surely help compare current and projected scenarios, taking into account home appreciation and rate changes.

I educate clients on historical trends and the complexities of market predictions highlighting the benefits of homeownership, such as:

- tax deductions,

- stable monthly payments (compared to rising rents), and

- equity building.

I rommend that buyers consult with their real estate agent or Reach Out to me Directly and other Caring Mortgage Advisors who can provide tailored advice based on your financial situation and market conditions.

Instead of waiting, do something, focus on individual readiness rather than market conditions! As I said, the best time to buy or even sellnis when you are ready. If buyers are financially prepared and have a stable income, they might benefit more from entering the market sooner rather than later.

While it’s natural to hope for lower rates, the financial realities often paint a different picture. Waiting for rates to drop can lead to missed opportunities and increased costs, making homeownership more challenging in the long run. By staying informed and making calculated decisions, buyers can position themselves for better financial outcomes, avoiding the pitfalls of the waiting game.

If you're considering buying a home, it's crucial to weigh the risks and rewards carefully. Remember, sometimes the best time to buy is when you are ready, not when the market seems perfect.

If you or you know anyone who need help or advice, please refer me to them and I'll be grateful!

Olajide Okunlola

672 998 2220

|

|

|

|

You may have been thinking of selling your house this spring, now is the perfect time to start getting it ready. With the market gearing up for its busiest time of year, it’ll be important to make sure your house shines bright among the competition.

Here are some valuable tips you can use to get your house

First impressions matter, and if your house is a mess, that can easily turn off potential buyers. Before listing, take the time to declutter and organize each room. Decluttering is about more than just tidying up – it’s about creating a sense of space and openness that allows potential buyers to envision themselves living in your home.

“Decluttering and organizing your space will go a long way in appealing to potential buyers. . . .decluttering will help the buyers see themselves living in your home. Less clutter inside a home also helps a place appear larger and cleaner, which should attract more buyers.”

The kitchen and bathrooms are focal points for many buyers, and often influence their overall opinion of the house. Ensure these spaces dazzle by giving them a thorough deep cleaning. Pay attention to details like scrubbing grout lines, polishing fixtures, and decluttering countertops. A sparkling kitchen and bathroom can leave a lasting positive impression on potential buyers.

Your home’s exterior is the first thing potential buyers see, so it’s important to make a good impression from the moment they arrive. A well-maintained yard not only enhances curb appeal, but also shows buyers the home has been well taken care of.

Take the time to spruce up your yard by mowing the lawn, trimming bushes, and clearing away any debris or dead plants. Remember, the goal is to create a welcoming environment that entices buyers to step inside and imagine themselves living there.

“A beautifully landscaped front yard can elevate an ordinary house into a charming home and will help homes sell faster and for more money.”

A skilled listing agent is your partner in minimizing stress when selling your home. Lean on your agent for advice on decluttering, staging, and enhancing your home’s appeal to potential buyers. Their insights into market trends and recommendations for reliable contractors and stagers are invaluable. A popular Realtor.com quote says:

“A good listing agent will help you price your home . . . recommend a photographer and stager to make it look its best, and put your home on the multiple listing service.”

By decluttering, deep cleaning, and tidying up your house, you can create a welcoming environment that resonates with buyers and increases your chances of a successful deal. Connect with a trusted real estate agent for advice on what you need to do to get your house ready to sell this spring.

As the weather warms up and flowers begin to bloom, the real estate market traditionally sees an uptick in activity during the spring season. This js where we are! If you're considering buying or selling a home, you might be wondering what kind of market conditions you can expect to encounter. Will it be advantageous for buyers, sellers, or will it strike a balance between the two? Let's quickly see into the current dynamics of this Spring 2024 real estate market

Determining whether it's a buyer's, seller's, or balanced market involves analyzing various factors such as:

1. Inventory levels,

2. Median home prices,

3. Interest rates, and

4. Buyer demand.

1. Buyer's Market: In a buyer's market, there are more homes for sale than there are buyers actively looking to purchase. This surplus of inventory typically leads to lower prices and more favorable terms for buyers. Sellers may need to be more flexible with their pricing and negotiation strategies to attract offers. Signs of a buyer's market include increasing days on market, declining prices, and a higher number of price reductions.

2. Seller's Market: Conversely, in a seller's market, there are more buyers than there are homes available for sale. This imbalance drives up competition among buyers, often resulting in bidding wars and homes selling for above asking price. Sellers have the advantage in this scenario, with the potential to receive multiple offers and sell their homes quickly. Low inventory levels, rising prices, and high demand characterize a seller's market.

3. Balanced Market: A balanced market occurs when the supply of homes is relatively equal to the demand from buyers. This equilibrium typically results in stable home prices and reasonable negotiation conditions for both buyers and sellers. While inventory may fluctuate slightly, it generally remains within a healthy range, preventing significant shifts in pricing dynamics.

As of spring 2024, the real estate market is exhibiting characteristics of both a seller's and balanced market in many areas. Despite not so low mortgage rates, there is still a strong buyer demand, while inventory levels remain tight in most regions. Sellers are benefitting from favorable selling conditions, including quick sales and competitive offers. However, buyers are also finding opportunities, particularly in areas where inventory is slightly higher or price growth has moderated.

Analysing the February and March 2024 data from the Canadian Real Estate Association, focusing on the sales-to-new-listings ratio (SNLR). This data was used to determine the sales-to-new-listings ratio (SNLR) for February and March, calculated by dividing the total sales by the number of new listings in each area of BC.

Honestly, the SNLR indicates the level of demand and supply in each area and can thus help local buyers and sellers determine local market conditions.

A sales to new listings ratio under 40% suggests a buyer’s market where new listings outweigh sales and buyers have more choice.

A sales to new listings ratio between 40% and 60% is a balanced market where demand and supply are at similar levels.

A sales to new listings ratio over 60% suggests a seller’s market where demand exceeds supply and sellers have the advantage.

While some areas like the BC interior and north has relatively stabilized in the balanced market region, Other markets like greater Vancover, Chilliwack and Fraser Valley areas are transitioning from a balanced market to a seller’s market, indicating increased interest in buying compared to the previous year.

Buyers: Act quickly when you find a property you like, as competition can be fierce. Get pre-approved for a mortgage to strengthen your offer, and consider being flexible with contingencies to make your offer more attractive to sellers.

Sellers: Price your home competitively based on market conditions and recent comparable sales. Showcase your home's best features through professional staging and high-quality listing photos. Be prepared to negotiate with multiple offers and consider all terms, not just the highest price.

While the spring real estate market may lean towards favoring sellers in some areas, there are still opportunities for both buyers and sellers to achieve their goals. By staying informed about local market trends and working with a knowledgeable real estate agent, you can navigate the current market conditions successfully. Whether you're buying or selling, it's essential to remain flexible and adaptable to maximize your chances of success in today's dynamic real estate landscape.

Thank you for reading, if you are looking to buy, sell or invest and you need some guidance please reach out to me and I'll be more than happy to lend some professional hands along the way, in order to make the journey smooth for you.

The First-Time Home Buyer Incentive helps qualified first-time homebuyers reduce their monthly mortgage payments without adding to their financial burdens.

The First-Time Home Buyer Incentive is a shared-equity mortgage with the Government of Canada, which offers:

The shared equity component of the incentive means that the government shares in both the upside and downside of the property value, up to a maximum gain or loss equal to 8% per annum (not compounded) on the Incentive amount from the date of advance to the time of repayment.

By obtaining the Incentive, the borrower may not have to save as much of a down payment to be able to afford the payments associated with the mortgage. The effect of the larger down payment is a smaller mortgage, and, ultimately, lower monthly costs.

The homebuyer will have to repay the Incentive based on the market value of the home at the time of repayment equal to the percentage (for example, 5% or 10%) of the original home value used to determine the Incentive, up to a maximum repayment amount equal to:

(i) where the home’s value has appreciated, the Incentive plus a maximum gain of 8% per annum (not compounded) on the Incentive amount from the date of advance to the time of repayment; or

(ii) where the home’s value has depreciated, the Incentive minus a maximum loss of 8% per annum (not compounded) on the Incentive amount from the date of advance to the time of repayment.

The homebuyer must repay the Incentive after 25 years, or when the property is sold, whichever comes first. The homebuyer can also repay the Incentive in full any time before, without a pre-payment penalty.

The First-Time Home Buyer Incentive has been discontinued.

The deadline for new or updated submissions for the First-Time Home Buyer Incentive is midnight ET on March 21, 2024.

Are you looking to end your Tenancy agreement with your tenant for your own use as the landlord? There is a way to do it right. In this blog I will be sharing some important insights for your learning.

A landlord may issue a Two Months Notice if the landlord wishes to regain possession of the rental unit, in good faith, for the landlord’s own occupancy or for occupancy by one or more of the landlord’s close family members.

First, let's define terms:

“Close family member” includes the landlord’s parents, spouse and children as well as the landlord’s spouse’s parents and children. Notably, neither the landlord’s siblings nor cousins fall within the definition of this term. However, if the landlord is a family corporation, the principle shareholder’s brother, sister or close family member who holds voting shares would be eligible to take over occupancy of the rental unit, as would the principle shareholder.

Where the tenancy is on a month-to-month basis, the landlord’s notice is effective not earlier than two months after the date the tenant receives the notice and its effective date must be on the day before the day of the month that rent is normally due. For example, if a tenant’s rent is due on the first day of each month and the landlord intends to evict the tenant by July, the landlord may seek to terminate the tenancy on June 30th and, if so, will have to provide the tenant with their notice by April 30th.

Where the tenancy is for a fixed-term, in addition to the rules described above, the effective date of the notice may not be earlier than the date specified as the end of the fixed-term.

The grounds for eviction require the landlord to be acting in good faith. Practically speaking, this means that the landlord must be acting with an honest intention and with no ulterior motive to defraud the tenant or to seek an unconscionable advantage.

In addition to the two months’ notice, a landlord seeking to end a tenancy to regain possession of the rental unit must provide the tenant, before the effective date of the notice, with monetary compensation equivalent to one month’s rent payable under the tenancy agreement. However, instead of having the landlord issue a separate payment for such compensation, the tenant may elect to simply withhold payment of rent for the final month of the tenancy.

Once served with a Two-Month Notice to End Tenancy, the tenant may challenge it by applying for dispute resolution within 15 days after receiving the notice. If the tenant fails to take any action within 15 days, the tenant is presumed to have accepted that the tenancy ends on the effective day of the landlord’s notice and must vacate the rental unit by that date.

Finally, if the landlord fails to take steps to accomplish the stated purpose for ending the tenancy (ie. to personally occupy or have a close family member occupy the rental unit) within a reasonable period after the effective date of the landlord’s two-month notice or if the rental unit is not used for that stated purpose for at least 12 months beginning within a reasonable period after the effective date of the notice, the landlord must pay the tenant a penalty equivalent to twelve-times the monthly rent payable under the tenancy agreement.

However, if the Residential Tenancy Branch determines that “extenuating circumstances” prevented the landlord from fulfilling their obligation under the Act to occupy the rental unit within a reasonable period of time after the effective date of the notice and/or for a minimum period of 6 months, the landlord may be excused from this requirement.

Thank you for taking time to read!

Should you need more guidance on how to proceed with any landlord tenant issues, please reach out to me directly on 672 998 2220

We will be discussing the trends and predictions for the real estate market in the year.

As 2024 kicks off full time, many factors are influencing the housing market, including interest rates, economic indicators, and demographic shifts. I'll be diving into what experts are forecasting for the year ahead and how it may impact you whether as a home buyer or seller.

Whatever category you find yourself, a first-time homebuyer, a real estate investor, or simply curious about the future of the housing market, this report will provide valuable insights and information to help you make informed decisions. Let's dive into it:

While we can't really forecast the future, we can use as it saw it's past share of twists and turns just as the housing market shifted.

Well, because prices are driven by supply and demand and we still have a low supply of inventory in the market, this means there will be upward pressure on home prices. Already there are slight home price gains. Somewhat easing inventory, slightly increasing transactions volume. All in all things are looking up for home prices are expected to see small but steady increases every year through 2028.

And while the percent of appreciation may not be as high as it was in recent years, what’s important to focus on is that we’ll see prices rise, not fall, for at least the next 5 years with 2024 looking at about a 2.6% increase. If you were worried home prices are going to fall, this is a big takeaway. Even though prices vary by local area, experts project they’ll continue to rise across the country Canada for years to come at a pace that’s more normal for the market.

With that in mind, bringing in these national insights as well as what’s happening in our Fraser Valley local market will help you see the bigger impact.

So, as a seller, selling your house appropriately so you can catch the eyes of serious buyers is important, especially in this mortgage rate environment. For buyers, with supply still tight, buyers will need to be flexible and willing to meet sellers halfway.

The past few years saw a lot of volatility in mortgage rates. Which leaves many wondering... what will happen with them in 2024? More than anything else, last year’s housing market was defined by high mortgage rates, reaching a 23-year high. But we’ve seen relief in the past few months as the recent Bank of Canada rate nouncements has made them flat e slowly trended down.

So, will mortgage rates continue to decline in 2024? No one can say for certain, but here’s what we know based historical trends. There’s a long-standing relationship between mortgage rates and inflation. Basically, when inflation is high, mortgage rates tend to follow suit.

Over the past year, inflation was up, so mortgage rates were as well. But inflation is easing now. And this is why the Bank of Canada has recently paused their rate hikes, which means many experts believe mortgage rates will continue their downward trend.

In fact, we’ve already started to see this decline in recent months. While the downward trend of both inflation and mortgage rates is promising, what you will have to brace for is that volatily is likely to continue going in 2024. Some ongoing variation is to be expected, but the anticipation is we’ll continue to see a downward trend this year.

Last year saw the lowest amount of homes sold in a decade. So, will we see activity pick up or are we in for another slower year? The strains on inventory due to rising homes prices as well as mortgage rates were felt nationwide this past year. Terms like “rate lock” and “affordability crisis” were prominent in headlines and articles about reasons why people had put their buying or selling plans on hold.

The short answer is no. While you may see headlines saying inventory is up, data also shows there are still signifcantly fewer homes for sale than there would usually be in a more normal market. However, what we’re seeing most is that this has become very hyper local. And while some cities in BC are seeing inventory declines, many are seeing the opposite: steady month over-month growth.

The market was no doubt thrown a lot of curveballs this year - namely high mortgage rates impacted by a wide variety of factors. However, as we start to see inflation cool and mortgage rates come down, it’s possible that prices will shoot up. Plus, it’s really not a matter of if but when we start to see that buyer and seller activity kick back up. So, the question becomes, what’s going to make an impact on those projections?

It all goes back to - you guessed it - mortgage rates.And although mortgage rates may remain volatile, their recent trend combined with what experts are saying indicate they could continue their downward trend in 2024. That would improve affordability for buyers and make it easier for sellers to move since they won’t feel as locked-in to their current, low mortgage rate.

Now that You Know what the market will look like in 2024, will you be willing to make the move?

Let's talk if you need some courage to take action!

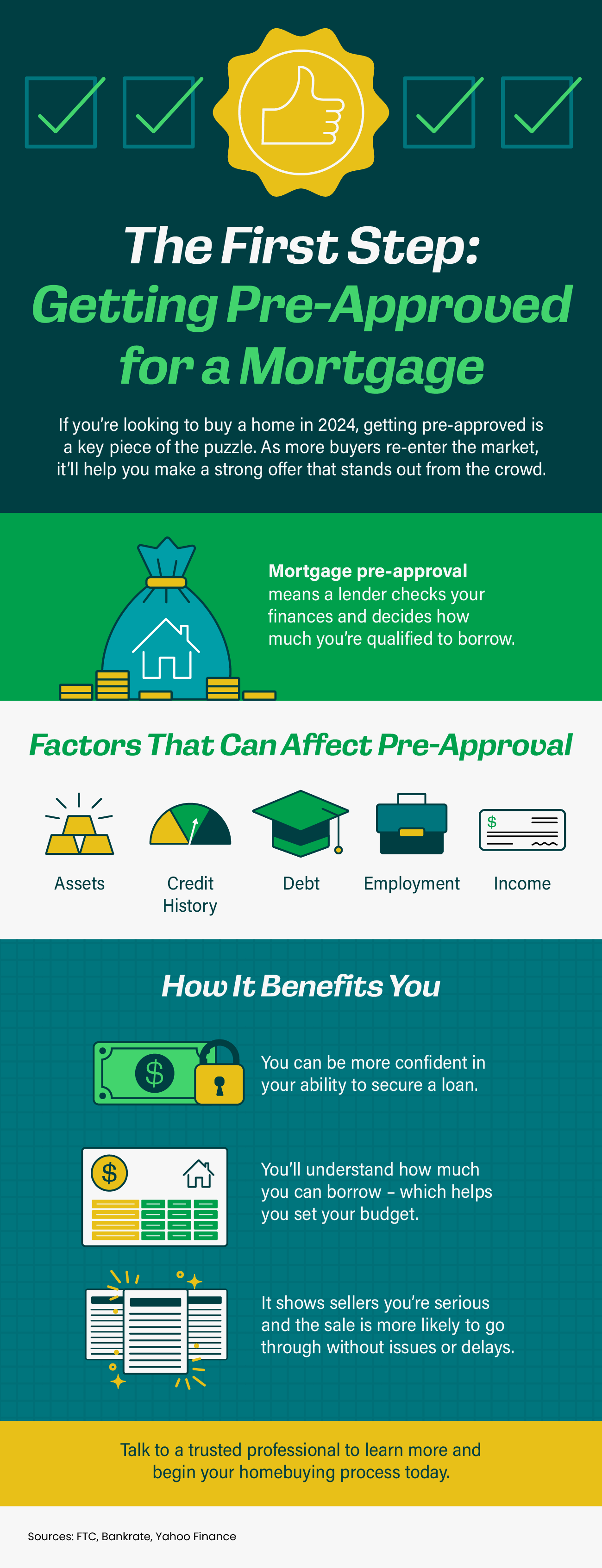

![First Things First: Getting Pre-Approved for a Mortgage [INFOGRAPHIC]](/wps/rest/64107/post/8118515/image.jpeg)

Thank you for taking the time read!

In this simple steps to Mortgage Application for First Time Home Buyers I will walk you through the information required when applying for a mortgage as a first time home buyer.

Purchasing your first home can be an overwhelming process, but we are here to simplify it for you. From gathering necessary documents to understanding the different types of mortgages available, I've got you covered.

Don't let the mortgage application process intimidate you - with the right guidance, you can navigate it smoothly. Let's dive in and learn everything you need to know about applying for a mortgage as a first time home buyer.

For your interest, these are the information that is normally required:

(You'll need to provide information for each person to be included on application)

Your Full Name:

Email (for each person):

Social Insurance #:

Birthdate:

Address:

Marital status:

Are you a Canadian Citizen or Permanent Resident of Canada?:

Do you own or rent your current home?:

Driver's license # and expiry date

Current monthly rent:

# of years at present address:

Your phone #:

Previous address (if at present address for less than than 2 yrs):

Email address:

Current Employer & phone:

Occupation:

# years with present employer:

Income (T4 income for past two years):

![How To Win as a Buyer in a Sellers’ Market [INFOGRAPHIC]](/wps/rest/64107/post/8118516/image.jpeg)

![How To Win as a Buyer in a Sellers’ Market [INFOGRAPHIC] | Simplifying The Market](https://files.keepingcurrentmatters.com/wp-content/uploads/2022/02/20220211-MEM.png)

Thank you for taking the time to read through.

The Bank of Canada maintained its overnight rate at 5 per cent this morning.

In the statement accompanying the decision, the Bank noted that economic growth is slow, wage pressures are easing, and the economy overall appears to be in a state of modest excess supply. On inflation, the Bank cited that shelter costs remain the largest contributor to inflation and that it expects headline CPI inflation to remain close to 3 per cent in the first half of this year before gradually falling back to its 2 per cent target.

March 6th 2024 - This morning's decision was much more about what the Bank is signaling for future meetings than the decision itself. All attention will now shift to April 10th, the Bank's next meeting and the first in which a rate cut is a real possibility. Although the economy flirted with recession in 2023, it has so far managed to avoid a lengthy contraction in output. However, economic growth does appear rather anemic and given substantial progress on bringing inflation toward 2 per cent, it is clearly time for the Bank of Canada to begin easing policy. We expect that the Bank will eventually lower its overight rate by 100 basis points this year, with the first rate cut happening in April or June.

There are interesting days ahead. If you have been on the sideline looking to sell or buy and you need some clarification on how to proceed, please reach out to me directly by text 672.998.2220 I'll be glad to answer all your burning questions...:)

Thank you!

For further readings please click here

Are you tired of constant home maintenance issues? You're not alone. Here are some simple hacks every homeowner should know to make their lives easier.

One of the most common issues homeowners face is a clogged drain. To easily unclog it, pour a mixture of vinegar and baking soda down the drain.

If you have squeaky doors, spray some WD-40 on the hinges for a quick fix.

To remove stubborn water stains on faucets, use a mixture of lemon juice and baking soda.

For a quick way to clean your microwave, place a bowl of water and vinegar inside and heat it up for a few minutes. The steam will loosen any dried-on food for easy cleaning.

To prevent dust buildup on ceiling fan blades, use a pillowcase to cover the blade and slowly pull it off. This will trap the dust inside the pillowcase.

By following these simple hacks, you can save time and money on home maintenance. Thanks for reading!

If you'll love to ask some specific real estate questions, you can reach out directly to me: 672.998.2220